Saudi Arabia Cloud Services Market Size

| Study Period | 2019 – 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 – 2030 |

| Market Size (2025) | USD 4.72 Billion |

| Market Size (2030) | USD 10.28 Billion |

| CAGR (2025 – 2030) | 16.85 % |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order |

Saudi Arabia Cloud Services Market Analysis

The Saudi Arabia Cloud Services Market size is estimated at USD 4.72 billion in 2025, and is expected to reach USD 10.28 billion by 2030, at a CAGR of 16.85% during the forecast period (2025-2030).

The Saudi Arabian technology landscape is undergoing a profound transformation as part of its broader economic diversification efforts. According to recent government data, technology investments account for 21.7% of all national technological expenditures, highlighting the kingdom’s commitment to digital advancement. This substantial investment has facilitated the creation of a robust digital infrastructure, with 141 government agencies already publishing over 6,442 open datasets. The integration of advanced technologies across various sectors has positioned Saudi Arabia as a pioneer in the MENA region for ICT readiness and cloud computing adoption.

The healthcare sector has emerged as a key adopter of cloud technologies, driven by the need for enhanced operational efficiency and improved patient care delivery. Recent surveys indicate that 48% of healthcare leaders in Saudi Arabia have either implemented or are currently implementing predictive analytics in their organizations. Healthcare providers are increasingly migrating from traditional infrastructure to cloud-based solutions, enabling seamless access to patient records, streamlined operations, and improved resource utilization. This transformation has been particularly evident in the deployment of multi-cloud solutions that facilitate secure data management and enhanced interoperability across healthcare facilities.

The financial services sector is witnessing a remarkable shift toward cloud-native technologies and digital transformation. Banks and financial institutions are incorporating advanced technologies such as artificial intelligence, machine learning, and cloud services to replace legacy hardware and software systems. The sector’s evolution is characterized by the implementation of hybrid multi-cloud architectures that balance cost, complexity, speed, and scalability while enabling new revenue streams. This transformation is particularly evident in the growing fintech sector, where cloud services are becoming fundamental to innovation and service delivery.

The manufacturing and industrial sector is experiencing significant cloud adoption, with over 10,000 industries spread across 40 different industrial cities embracing digital transformation. The sector, which accounts for 11% of the country’s GDP with a growth rate of 10% year-over-year, is leveraging cloud services to optimize productivity and gain deeper insights into factory performance. The implementation of Industrial Internet of Things (IIoT) solutions and automation processes is driving the need for robust cloud infrastructure that can support real-time data analytics and operational efficiency improvements.

Saudi Arabia Cloud Services Market Trends

Government Policies and Initiatives

The Saudi government has implemented comprehensive policies to accelerate cloud adoption across both public and private sectors. The introduction of the Cloud First Policy in 2019 marked a significant milestone in the kingdom’s digital transformation journey, aimed at expediting the transition of government organizations from traditional IT systems to cloud-based alternatives. This policy acknowledges the multiple benefits of cloud computing, including enhanced agility, reliability, cloud security, and innovation potential, while serving as a cornerstone for the kingdom’s broader digital transformation agenda.

The Communication and Information Technology Commission (CITC) has further strengthened the regulatory framework through the implementation of the Cloud Computing Regulatory Framework (CCRF) v3. This framework defines clear expectations for cloud service providers and their clients, demonstrating the government’s commitment to creating a robust ecosystem for cloud services. The policy has already shown significant results, with the country experiencing a 16% growth rate in cloud services since the launch of its Cloud First Policy in 2019.

Economic Benefits Leading to Cloud Adoption

The economic landscape in Saudi Arabia is experiencing a remarkable revival, with the International Monetary Fund projecting significant growth in real GDP. This economic expansion is creating a fertile ground for cloud adoption as businesses seek to optimize operations and reduce capital expenditure. The strong financial system, robust banking industry, and massive government corporations based on a highly skilled Saudi workforce are driving the adoption of cloud services across various sectors.

The public sector’s budget management demonstrates the government’s commitment to digital transformation, with a projected budget surplus of 2.5% of GDP (approximately SAR 90 billion) in 2022. This financial stability, combined with reduced public debt targets of SAR 938 billion (25.9% of GDP), enables sustained investment in cloud infrastructure and services. The government’s strategic allocation of resources, including a planned spending of SAR 955 billion, provides a strong foundation for continued cloud adoption and digital transformation initiatives.

Increasing Penetration of Technology Giants

Major technology companies are significantly expanding their presence in Saudi Arabia, recognizing the growing demand for agile and scalable IT infrastructures. In August 2022, Alibaba Cloud made a strategic entry into the Saudi market through a joint venture under the Saudi Cloud Computing Company (SCCC), demonstrating the increasing interest of global tech giants in the region. This venture includes the establishment of two data centers in Riyadh, offering various public cloud computing solutions to meet growing corporate demand across sectors.

The market is witnessing a surge in strategic partnerships and investments from leading technology providers. For instance, in February 2022, Oracle Corporation chose Al Ekhbariya, the broadcast station in Saudi Arabia, to implement Oracle Cloud Infrastructure (OCI) for digitalizing its content and improving user experience. Similarly, Microsoft has been actively expanding its cloud services in the region through partnerships with local entities, contributing to the development of a robust cloud ecosystem. These developments are accompanied by significant investments, such as Alibaba Cloud’s commitment of USD 500 million for two new data centers in Saudi Arabia.

Segment Analysis: By Deployment

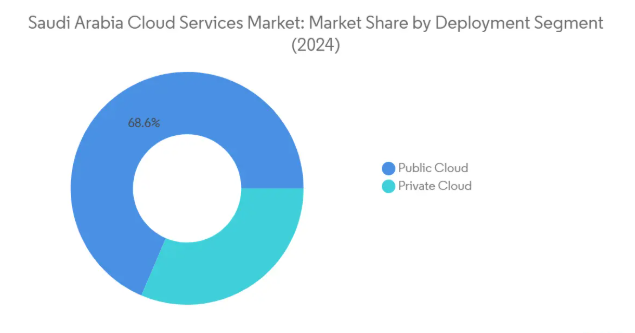

Public Cloud Segment in Saudi Arabia Cloud Services Market

The public cloud segment maintains its dominant position in the Saudi Arabia cloud services market, commanding approximately 69% market share in 2024. This substantial market presence is driven by the increasing adoption of Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), and Infrastructure-as-a-Service (IaaS) solutions across various industries. The segment’s growth is further bolstered by the Saudi government’s Cloud First Policy and the increasing presence of global cloud service providers in the region. Major technology companies like Google Cloud, Amazon Web Services, and Microsoft Azure have established data centers in Saudi Arabia, offering enhanced services and local data residency options. The public cloud’s popularity stems from its cost-effectiveness, scalability, and ability to provide organizations with access to advanced technologies without significant upfront investments.

Private Cloud Segment in Saudi Arabia Cloud Services Market

The private cloud segment is experiencing the fastest growth trajectory in the Saudi Arabia cloud services market, with an expected growth rate of approximately 19% during 2024-2029. This accelerated growth is primarily driven by increasing demands from organizations requiring enhanced security, compliance, and data sovereignty. The segment’s expansion is particularly notable in sectors handling sensitive information, such as government agencies, financial institutions, and healthcare organizations. The growth is further supported by the implementation of stringent data protection regulations and the need for customized cloud solutions. Private cloud adoption is also gaining momentum as organizations seek greater control over their IT infrastructure while maintaining the benefits of cloud computing, such as improved resource utilization and operational efficiency.

Segment Analysis: By End-User Industry

Financial Services Segment in Saudi Arabia Cloud Services Market

The financial services segment holds a dominant position in the Saudi Arabia cloud services market, commanding approximately 23% market share in 2024. This leadership position is driven by the dramatic shift in how customers conduct financial transactions in the Kingdom, with digital transactions becoming the new norm. Financial organizations in Saudi Arabia are actively transitioning from legacy hardware and software to advanced technologies such as AI, ML, and cloud services. The sector’s growth is further supported by the Saudi Ministry of Finance’s FinTech Strategy Implementation Plan, which aims to establish the kingdom as a fintech hub. Banks and financial institutions are incorporating cloud-native technologies to respond to evolving business demands, with many institutions partnering with innovative cloud service providers to foster fintech growth, innovation, and collaboration across the financial services industry.

Healthcare Segment in Saudi Arabia Cloud Services Market

The healthcare segment is emerging as the fastest-growing sector in the Saudi Arabia cloud services market, with an expected growth rate of approximately 18% during 2024-2029. This remarkable growth is primarily driven by the Ministry of Health’s aggressive digital transformation initiatives and the deployment of multi-cloud solutions to optimize operations across the country’s healthcare providers. Healthcare institutions are increasingly adopting cloud services to enable providers to switch from using labor-intensive, energy-hungry servers to manage their IT operations securely from the cloud. The sector’s growth is further bolstered by various cloud service providers working with the Ministry of Health and private healthcare providers to implement innovative technology solutions, protected by robust cybersecurity measures, that streamline patient care delivery regardless of location.

Remaining Segments in End-User Industry

The other significant segments in the Saudi Arabia cloud services market include Government and Defense, Manufacturing and Construction, Oil, Gas, and Utilities, and other industries. The government and defense sector is particularly notable due to the kingdom’s cloud-first strategy and comprehensive digitization initiatives. The manufacturing and construction segment is benefiting from the Future Factories Program, which aims to transform thousands of factories with automated and advanced manufacturing technologies. The oil, gas, and utilities sector is experiencing increased cloud adoption through various partnerships with global technology providers, while other industries such as education, retail, and telecommunications are also showing significant growth potential through digital transformation initiatives.

Saudi Arabia Cloud Services Market Overview

Top Companies in Saudi Arabia Cloud Services Market

The cloud services market in Saudi Arabia is dominated by major global technology companies that are actively expanding their presence through strategic partnerships and infrastructure investments. These players focus on continuous product innovation by enhancing their offerings with advanced technologies like AI, machine learning, and IoT integration to meet evolving customer needs. Companies demonstrate operational agility by establishing local data centers, forming joint ventures with cloud service providers in Saudi Arabia, and tailoring solutions for specific industry verticals such as financial services, healthcare, and government sectors. Strategic moves include significant investments in research and development, strengthening partner ecosystems, and developing specialized cloud solutions aligned with Saudi Vision 2030 objectives. Market leaders also prioritize expansion through multiple approaches, including building new facilities, acquiring local companies, collaborating with government entities, and creating comprehensive training programs to address the skill gap in the region.

Dynamic Market with Strong Growth Potential

The Saudi cloud services market exhibits a mix of global technology conglomerates and specialized local providers, with international players holding dominant positions through their established technological capabilities and extensive resource networks. Market consolidation is increasingly evident as major cloud providers in Saudi Arabia acquire smaller specialized firms to enhance their service portfolios and gain local market expertise. The competitive landscape is characterized by strategic partnerships between global cloud giants and Saudi telecommunications companies, creating robust hybrid offerings that combine international expertise with local market knowledge.

The market demonstrates strong competitive intensity with companies actively pursuing cloud market share through various strategies, including price optimization, service customization, and enhanced local presence. Merger and acquisition activities are primarily driven by the need to acquire specialized capabilities in emerging technologies, enhance geographical coverage, and strengthen vertical-specific solutions. Local players are increasingly becoming attractive acquisition targets for global companies seeking to establish stronger footholds in the Saudi market, while also serving as strategic partners for delivering solutions that comply with local data sovereignty requirements.

Innovation and Localization Drive Market Success

Success in the Saudi cloud services market increasingly depends on providers’ ability to balance global capabilities with local market requirements. Incumbent providers must focus on developing industry-specific solutions, strengthening their partner ecosystems, and maintaining high standards of data security and sovereignty to maintain their market positions. Companies need to invest in local talent development, establish robust customer support infrastructure, and demonstrate long-term commitment to the Saudi market through continuous infrastructure investments and alignment with national digital transformation initiatives.

For contenders looking to gain cloud market share, the focus should be on identifying and serving underserved market segments, developing specialized solutions for specific industries, and building strong relationships with local partners. The relatively low risk of substitution due to high switching costs provides stability for established players, while regulatory requirements around data localization and privacy create opportunities for providers who can effectively navigate these requirements. Success also depends on providers’ ability to address the concentrated nature of key end-user segments, particularly government and large enterprises, while maintaining flexibility to serve the growing small and medium enterprise market.

Saudi Arabia Cloud Services Market Leaders

-

- Google LLC (Alphabet Inc.)

- Amazon Web Services Inc. (Amazon.com, Inc.)

- Alibaba Cloud (Alibaba Group Holding Limited)

- Microsoft Corporation

- Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Saudi Arabia Cloud Services Market News

- February 2023: In order to meet growing demand for its cloud services, Oracle plans to set up a 3rd Public Cloud Region in Saudi Arabia. Oracle’s planned investment of USD 1.5 billion in the Kingdom to upgrade cloud infrastructure capabilities is part of this new cloud region, which will be set up in Riyadh. The Oracle Cloud Riyadh Region will likely be added to the current Oracle Cloud Jeddah Region and the proposed Oracle Cloud Region in the future metropolis of NEOM.

- February 2023: At the LEAP23 conference, Google Cloud announced a partnership with Lean Business Services, which offers Digital Health solutions. Lean used Google Cloud’s Apigee solution in Saudi Arabia to develop a Digital Platform for Medical Institutions that will likely enable them to deliver secure healthcare services. Google Cloud claims that this collaboration enabled Lean to develop APIs and authenticate health institutions and individuals in order to use telemedicine.

Saudi Arabia Cloud Services Market Industry Segmentation

Cloud services are a broad category of on-demand services supplied to businesses and users through the Internet. These services are intended to enable simple, low-cost access to applications and resources that do not require internal infrastructure or hardware. Cloud computing vendors and service providers oversee all aspects of cloud services. A business does not need to host apps on its in-house servers as they are made available to clients from the providers’ servers.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The scope of the study includes deployment and end-users. In addition, the study provides cloud service adoption trends and crucial vendor profiles. The study further analyses the overall impact of COVID-19 on the ecosystem.

The saudi arabia cloud services market is segmented by deployment (public cloud [software-as-a-service, platform-as-a-service, infrastructure-as-a-service], private cloud), end-user industry (oil, gas & utilities, government & defense, healthcare, financial services, manufacturing & construction). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Deployment | Public Cloud | Software-as-a-Service (SaaS) |

| Platform-as-a-Service (PaaS) | ||

| Infrastructure-as-a-Service (IaaS) | ||

| Private Cloud | ||

| By End-User Industry | Oil, Gas, and Utilities | |

| Government and Defense | ||

| Healthcare | ||

| Financial Services | ||

| Manufacturing and Construction | ||

| Other End-User Industries |

Saudi Arabia Cloud Services Market Research FAQs

The Saudi Arabia Cloud Services Market size is expected to reach USD 4.72 billion in 2025 and grow at a CAGR of 16.85% to reach USD 10.28 billion by 2030.

In 2025, the Saudi Arabia Cloud Services Market size is expected to reach USD 4.72 billion.

Google LLC (Alphabet Inc.), Amazon Web Services Inc. (Amazon.com, Inc.), Alibaba Cloud (Alibaba Group Holding Limited), Microsoft Corporation and Oracle Corporation are the major companies operating in the Saudi Arabia Cloud Services Market.

In 2024, the Saudi Arabia Cloud Services Market size was estimated at USD 3.92 billion. The report covers the Saudi Arabia Cloud Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Saudi Arabia Cloud Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Saudi Arabia Cloud Services Market Research

Our research encompasses various segments including software as a service, platform as a service, and infrastructure as a service, with special focus on emerging trends in cloud computing and cloud technology adoption across Saudi Arabia. The report includes thorough analysis of key market indicators, regulatory frameworks, and strategic developments by leading cloud service providers in saudi arabia, helping stakeholders make informed decisions.

Our consulting expertise extends beyond traditional market research to provide actionable intelligence in the cloud solutions landscape. We assist organizations in technology scouting for emerging cloud technologies, conducting thorough competition assessment of cloud providers in saudi arabia, and developing go-to-market strategies tailored for the Saudi market. Our capabilities include B2B surveys with enterprise cloud users, data aggregation and visualization of cloud adoption patterns, and comprehensive analysis of customer needs and behavior in the saudi cloud ecosystem. We also provide strategic support in partner identification and assessment, helping global cloud providers establish and expand their presence in the Saudi Arabian market.